For over ten years, passive investing has impacted global asset management significantly. The attraction of low fees, ease of use, and strong performance has fueled the rise of index-tracking strategies. Nevertheless, this success depicts a more complex scenario characterized by concentration risk and the opportunity cost tied to limited engagement with emerging growth sectors.

As market conditions evolve, these risks become apparent, leaving investors adhering to index strategies exposed to prior high performers. In such contexts, active management clearly demonstrates its advantage through selective allocation, risk management, and the ability to exploit new opportunities as they emerge.

Read/listen:

The war effect: The real story versus the market story

Outperforming the index in 2026

Generally, passive strategies mirror indices weighted by market capitalization, which means larger firms have a greater influence on the index’s performance.

Strong stock price performance inherently increases that exposure. The U.S. exemplifies this phenomenon with a small array of tech behemoths—the Magnificent 7: Alphabet, Amazon, Apple, Meta Platforms, Microsoft, Nvidia, and Tesla—responsible for a substantial share of market returns.

Their supremacy arises from true innovation, especially in AI and digital infrastructure, yet this dependence on a limited number of companies and themes makes index performance increasingly susceptible.

Source: Bloomberg as of 31 March 2026. Based on research from Defiant Capital Group.

ADVERTISEMENT

CONTINUE READING BELOW

A similar trend is observed in South Africa. After years of lackluster performance, the equity market has bounced back, but much of this rise is limited to a few sectors, notably precious metals firms benefiting from increasing commodity prices.

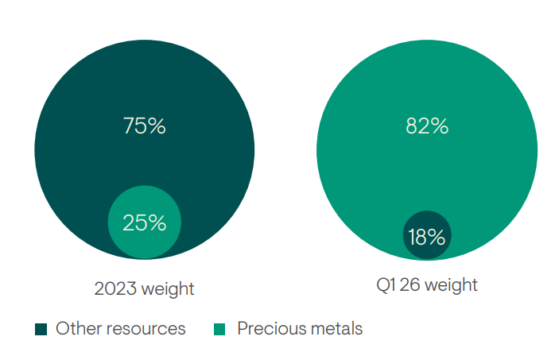

Among the top 25 companies in the FTSE/JSE All Share Index (Alsi), which make up about 75% of the index, resources surged from 22% to 31.3% in the last two years.

Interestingly, 25.6% of the 31.3% is attributed to just seven precious metals firms. Gold Fields and AngloGold Ashanti alone comprised 14.6% of the entire index by March 2026, a substantial increase from 5.5% in 2023.

While concentration isn’t inherently detrimental if key companies continue to excel, it does mean that index-tracking portfolios increasingly depend on a select few firms. When leadership changes, as it inevitably will, the effects on passive-heavy portfolios can be significant.

Watch: ‘The risks and opportunities you can’t overlook’ – Ninety One’s Hendrik du Toit

The global economy has also undergone substantial structural changes. Technological disruption, geopolitical shifts, and evolving supply chains are reshaping industries and altering competitive advantages. Innovations in artificial intelligence and automation are accelerating these transformations while nations and businesses reconsider their trade relations, energy security, and strategic priorities.

Supply chains are now focusing on regional resilience rather than mere cost efficiency. These dynamics account for much of the current market leadership while paving the way for new winners and themes to emerge.

ADVERTISEMENT:

CONTINUE READING BELOW

This is crucial for investors. Passive strategies often reinforce exposure to established leaders, whereas active managers can pivot towards fresh opportunities, respond to risks, and adjust portfolios as market leadership evolves.

Active vs passive debate

The discourse around active versus passive investing is commonly presented as a binary choice; however, in reality, the most effective portfolios typically blend both. Passive strategies offer efficient access to broad market exposure and can act as a strong foundation, while active strategies enhance prospects for superior returns, effective risk management, and adaptable capital allocation.

The essential question isn’t whether passive investing is successful—it is—but rather how much passive exposure is appropriate in the current environment and when to consider boosting allocations to active strategies.

Source: Bloomberg, as of 31 March 2026. Based on the top 25 stocks listed on the FTSE/JSE Alsi.

Current market dynamics indicate that the opportunity landscape for active investors is expanding. The concentration in primary equity indices has intensified, making returns increasingly dependent on a relatively small set of companies.

Additionally, divergence in valuations and growth outlooks across sectors and firms has widened, resulting in greater variability in potential outcomes.

ADVERTISEMENT:

CONTINUE READING BELOW

At the same time, the global economy is adapting to technological disruption, geopolitical transformations, and changes in supply chains.

Periods marked by concentration, dispersion, and structural change often favor investors capable of evaluating companies independently and allocating capital wisely. Passive investing remains a valuable tool for gaining broad market access, yet it also reflects the current state of the market, illustrating its concentrations, imbalances, and momentum.

Read:

Investors seek hedges as conflict disrupts long-standing strategies

A fund charging 6% fees? [Dec 2025]

In a swiftly changing environment, excessive reliance on index exposure risks tying portfolios too closely to past high performers. Increasing allocation to disciplined, research-driven active strategies can reduce concentration risk, uncover emerging opportunities, and adapt as market leadership transforms.

We assert that the upcoming phase of the cycle necessitates a conscious shift towards active management, combined with the adaptability to manage risks more effectively and seize new opportunities as they arise. Stay tuned for the next part of this series, where we will explore key assumptions and misconceptions about active and passive investing.

Siobhan Simpson is Head of SA Unit Trusts at Ninety One.